Charts on the Street is our effort to go beyond Bluekurtic’s own research and highlight insights from across the investment community. Each day, we curate charts from analysts, strategists, researchers, and institutions that are publicly available and we believe are worth reviewing.

The inclusion of a chart does not imply that Bluekurtic agrees with its conclusions, forecasts, or investment views. Our goal is to present a broad range of perspectives and research that may help investors better understand the market environment. These charts are not produced by Bluekurtic, and full credit belongs to their original authors.

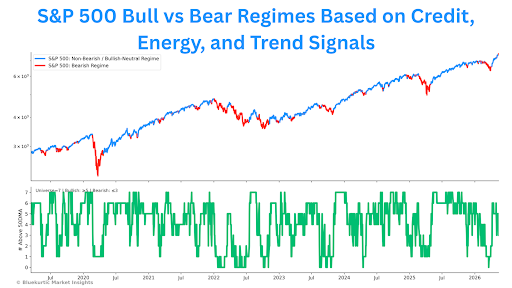

1 – @neilsethinew: Citadel’s Rubner: Over the past two weeks, the market has worked through many of the positioning excesses that concerned us entering July. Retail demand remains exceptionally resilient, systematic headwinds have eased, market leadership is broadening, financing conditions have improved, and valuations have become more attractive. The market’s attention now shifts from positioning back to fundamentals. The next two weeks will determine whether fundamentals can sustain the rally. Market leadership is broadening. Rather than exiting the asset class, investors are reallocating within equities. This rotation has become particularly evident on days when the index is weaker. Since the start of June, 9 of the last 14 S&P 500 down days (64%) have seen a majority of index constituents finish higher. Over the past year, that has occurred on just 32% of S&P 500 down days. Average breadth on down days has nearly doubled. Over the last 20 SPX selloffs, an average of 239 constituents finished higher, compared to a 20-year average of 133.

2 – @TheStalwart: According to Bank of America’s new fund manager survey, investors haven’t been this under-exposed to consumer stocks in over 20 years

3 – @LanceRoberts: According to Citadel Securities, retail investors remain the strongest structural buyers of US equities, with average daily net buying running at 3.2 times the historical monthly average, making July 2026 the second-strongest month since January 2020 and the strongest July for retail inflows. h/t @soberlook

4 – @JTheretohelp1: Retail is increasingly using options and selling more single stocks, signaling that the cohort has become pickier, chasing specific market themes rather than having broad conviction in benchmark indexes. — Citadel Securities I completely agree with Citadel! Their data on the attached chart supports the thesis. Options are currently controlling short-term movements in these markets. But never forget: macro and valuations still rule in the long run! Stay agile out there, friends! Source: Citadel Securities

5 – @VrntPerception: Pretty epic momentum unwinds so far in 3Q2026

6 – @JTheretohelp1: Crazy Chart of the Day! Hyperscaler credit stress (measured by the spread over US Treasuries) has reached its highest level since Goldman Sachs launched the basket in February. Note: Credit spreads in attached chart are inverted! Hence, right side up, they’re blowing out! Source: Goldman Sachs

7 – @intangiblecoins: an enormous amount of old BTC came online and moved onchain in 2024 and 2025, rivaled only by 2017 this ‘great distribution’ is mostly over and 2026 is on pace to see less than half the amount of awakened coins as last year

8 – @sam_gatlin: The smart money keeps selling bonds as price looks poised to fall off a cliff

9 – @BrianSozzi: The slow build toward Nvidia earnings:

10 – @zerohedge: Morgan Stanley also expects 80GW in new compute coming online from now until 2028. That translates to $4-$8TN in capex spending in just 3 years, all of which has to be funded with debt and equity (no more positive FCF).

11 – @junkbondinvest: The maturity wall always rolls. That’s basically the entire history of leveraged credit. 2028 is next up. Except there’s a real software concentration in the ’28/’29 bucket this time.

12 – @BrianSozzi: Hopes for an economic boom are on the rise:

13 – @TimmerFidelity: One big difference between now and then is that today’s fundamentals are backing up the valuations. While the 5-year CAPE ratio above raises eyebrows, booming earnings are so far keeping valuations in check. In fact, the chart below showing the forward P/E against high yield credit spreads suggests that valuations are quite reasonable today.

14 – @SteveRattner: The Strait of Hormuz is closed again — before it ever fully reopened. That is bad news for oil prices and inflation as a huge portion of global oil supply is stuck in the Gulf. My @Morning_Joe Chart

15 – @TimmerFidelity: With all the talk of semiconductor ETFs captivating the fast money, I can’t help but keep an eye on the dot com analog. I’m sure this analog will break down at some point (as all analogs do), but so far it has continued to be spot on, both in terms of price and the 5-year CAPE ratio.

16 – @GroupFinom: Believe it or not, CAPEX may have already peaked. Consensus analysts estimates for CAPEX spend in the forward quarters shows deceleration, not acceleration.

17 – @GroupFinom: Just eclipsed the amount of new stock supply overhead relative to 2021 and 2nd most in history relative to any calendar year since 1970. Since June, this has proven somewhat a headwind for markets, has not proven harbinger of doom all by itself.

18 – @JavierBlas: Excluding any US-Iran talks about Hormuz, China remains the most important factor for oil prices for the next 60 days or so. All eyes on Beijing. Ex-China Asian oil imports have recovered to normal levels, within the 2023-2025 range. What China does next is crucial.

19 – @felixavp: More evidence that peak hawkishness is behind us. Our Dual Mandate Surprise Index is rolling over, pointing to cresting front-end yields. Tighter FCs also suggest US economic surprises will keep moderating, but it’s about less upside surprise, not contraction.

20 – @GinaMartinAdams: Much has been written about the wealth and income gap that has developed among US households over the last several years, and the impacts of this gap on household spending patterns. However, the financial consequences of the k-shaped economy are now showing up as well. The consequences of a k-shaped economy, where the upper tier has accumulated financial assets and the lower tier has accumulated financial liabilities, are starting to show up in consumer credit markets. Credit card delinquencies broadly are near a level last reached during the 2008 financial crisis, but closer to longer term average as far as commercial bank books are concerned. Autos confirm the story from credit cards that subprime borrowers are under strain. If the trend persists, we may see delinquencies spread through medical bills, utility payments, and eventually mortgages. This fundamental dynamic impacting underlying collateral is amplified by a structural supply/demand mismatch in ABS broadly, which adds to the relative yield found in the ABS market vs more traditional areas of fixed income markets. As these delinquencies make their way into charge-offs, the ABS market may increasingly become a center of strain in fixed income. Due to the highly idiosyncratic nature of the market, however, such a strain should also present opportunities for active managers. @HB_Wealth

21 – @PeterBerezinBCA: Peak optimism?

22 – @neilsethinew: BofA clients also accelerated their buying of large caps while continuing to buy small caps at a record pace.

23 – @TimmerFidelity: Of course, the main event this week will be earnings season. The growth estimate for Q2 is +23%, which seems like a high hurdle to beat. Last quarter the estimate started at 14% and doubled during reporting season, so we’ll see what happens. My guess is that companies will beat as usual, but maybe less so than in the past. Note the two orange lines below, which were the 2018 quarters that started high and beat by only a little.

24 – @MacroCharts: One of the most important charts I’m watching: *Plus what it means for asset allocation today, and opportunities/risks. These are massive themes that could dominate the rest of 2026…

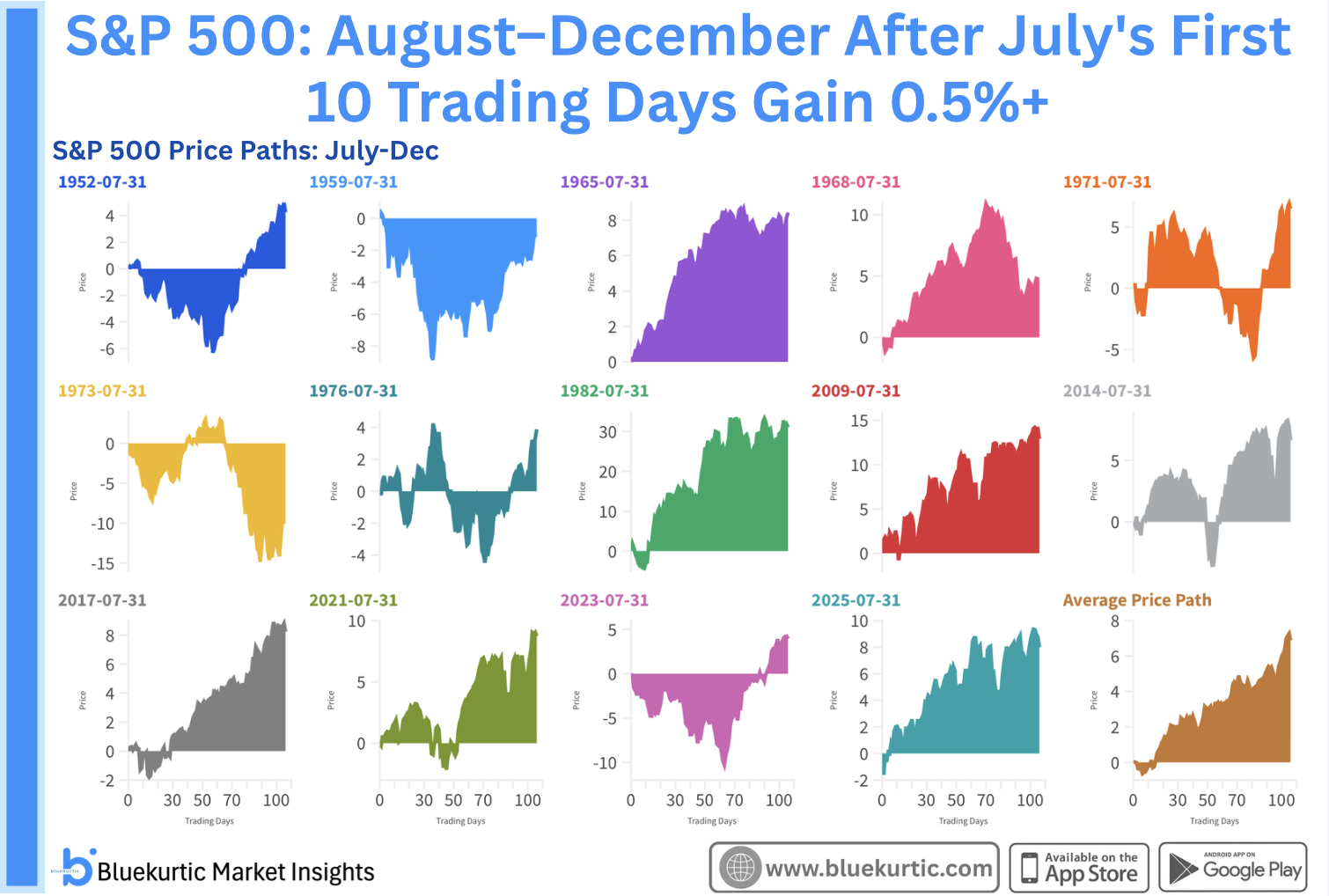

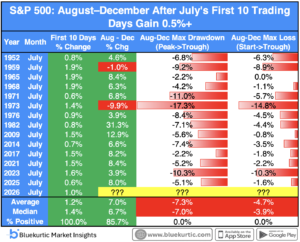

The S&P 500 closed out the first 10 trading days of July up roughly 1%. Looking back at every year since 1950 where that opening stretch gained 0.5% or more, the setup that follows tends to favor the bulls.

Across the fourteen prior instances of a strong first ten days in July, the S&P 500’s performance from August through December was negative only twice, in 1959 and 1973. Every other year finished the back half of the year higher, putting the historical hit rate at close to 86%. The average gain across all cases was 7.0%, with a median of 6.7%.

Just as important as the direction is how rough the ride got along the way. In no instance did the index suffer a drawdown of 20% or more between August and December. The worst case by far was 1973, which saw a peak to trough decline of 17.3%, a year that also happened to be one of the two negative outcomes.

Narrow the sample down to years where the S&P actually finished the period positive, which is our base case for the second half of this year, and the drawdowns get noticeably shallower. Most of those years stayed in single digits, with only 1971 and 2023 breaking into double digits peak to trough decline despite ending the period positive. The rest of the positive years clustered closer to the 2% to 10% range, reinforcing the idea that a strong start to July has historically come with a manageable amount of chop rather than a serious breakdown.

Our base case remains a drawdown of less than 10% in the S&P 500 through the second half of the year, and this pattern lines up with that view. It doesn’t guarantee anything, fourteen instances is a small sample and every cycle carries its own risks, but the historical tendency after a strong opening stretch in July has been continuation with limited downside, not a sharp reversal.

We’re maintaining our year end target of 8100 for the S&P 500, first set in December 2025. Nothing in this setup changes that view. If anything, the historical pattern here adds a bit more support to the case that this rally has room to keep building through year end, even if there’s a pullback along the way.

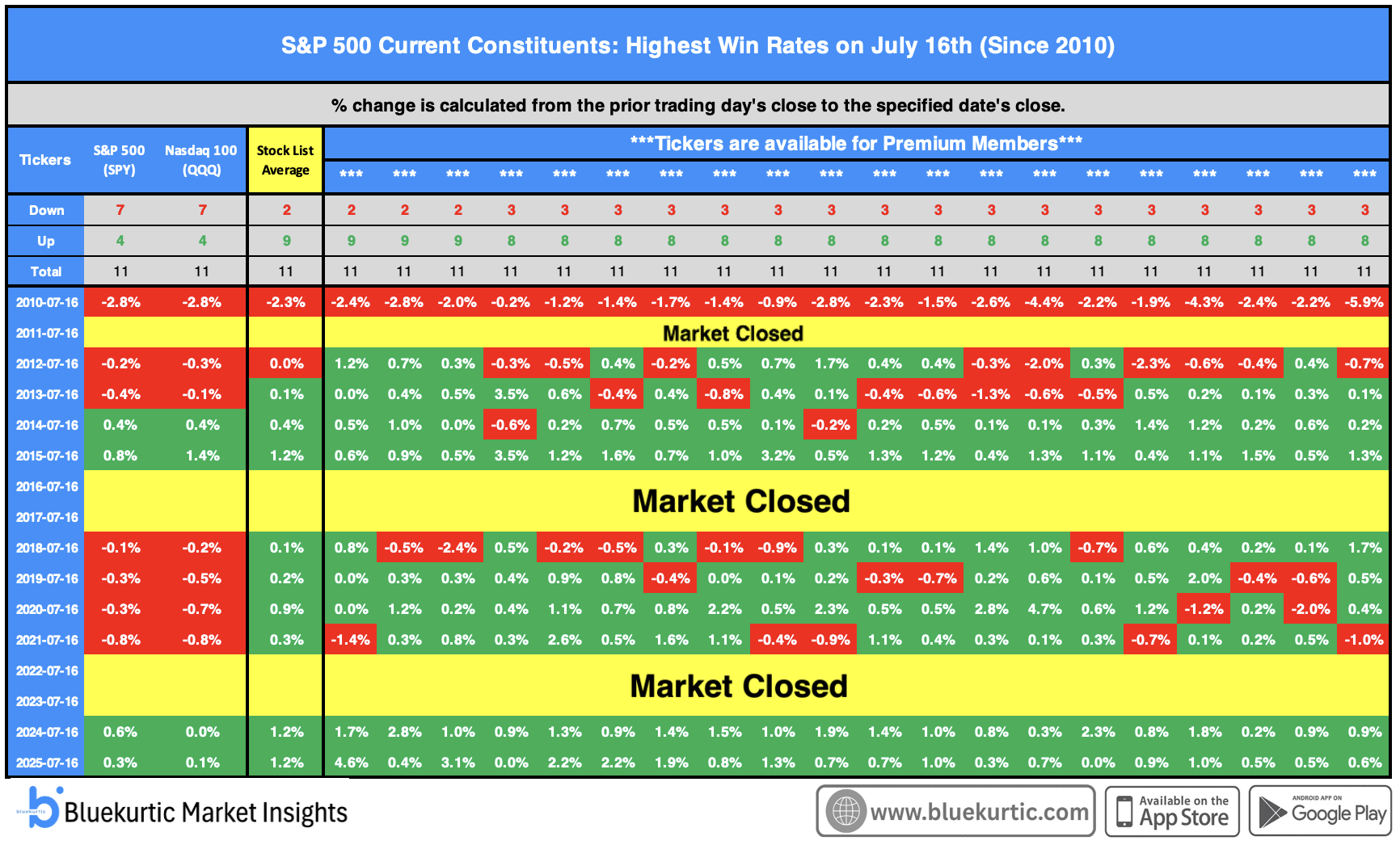

It’s a long list for the 16th. Since 2010, 3 stocks have been positive on 9 of 11 cases.

An equally weighted portfolio of these stocks has finished negative only twice on the day since 2010.

Note: Our Alpha Stock List is published every trading day, regardless of whether we identify stocks that meet our highest conviction standards. The objective is to highlight stocks with the strongest historical positivity rate for that specific calendar date. It is intended as a supporting research tool for active traders and should not be interpreted as a recommendation to buy or sell any security.

The portfolio’s average historical performance is provided solely for reference to illustrate how the group has performed collectively on that date in the past. Historical performance does not guarantee future results, and not every day’s list represents a high-conviction opportunity. Please conduct your own research before making any investment decisions.

For investors seeking our highest-conviction ideas, Premium Plus members receive access to our Berry Picks model portfolio under the Model Portfolio section. Berry Picks are selected from more than 30 proprietary research themes, with preference given to stocks that consistently appear across the greatest number of themes.

None of the stocks listed constitute investment advice.

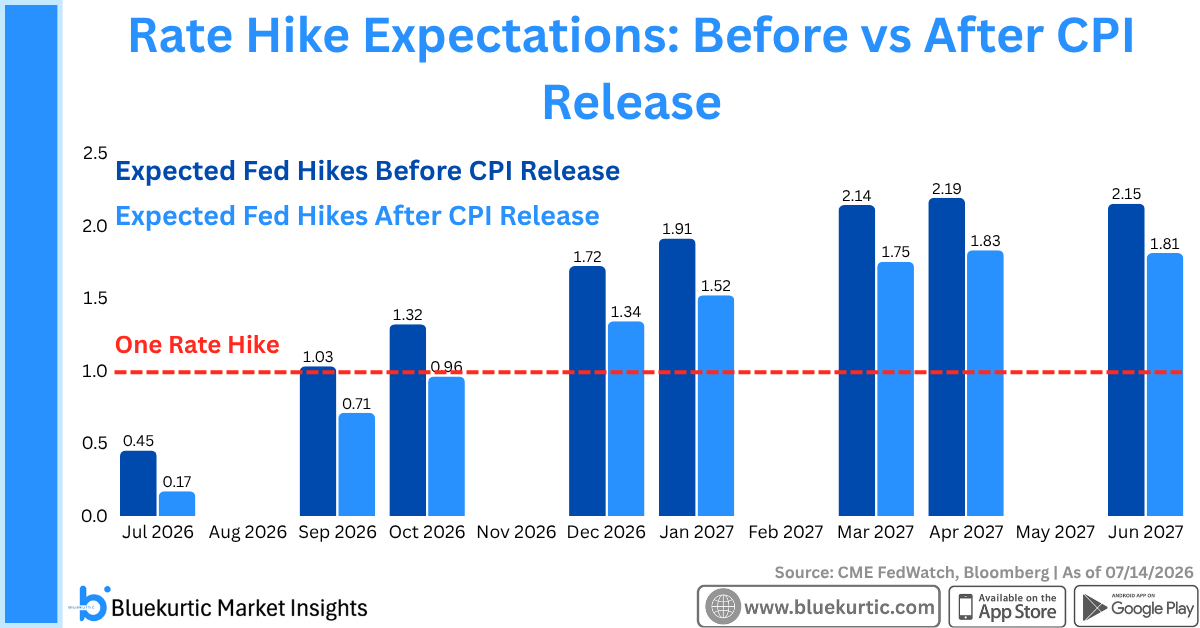

Yesterday’s thesis is playing out. Rate hike odds fell after the CPI print, and the S&P found room to push higher. June inflation came in soft, the first monthly decline since 2020, and it caught a market that had been leaning hawkish off guard. Headline CPI landed at 3.5% annually, below the 3.8% economists expected, with core inflation undershooting too. Two year yields dropped as much as 14 basis points intraday, the sharpest move since August, stocks caught a bid, and the dollar weakened broadly. Futures pricing pushed the likely timing of the next hike out to September or October.

That’s the setup working in the market’s favor. Lower hike odds, more room for equities to run.

There was some pushback in the afternoon. Fed Chair Warsh’s testimony leaned firmer than the morning’s data alone would suggest, and two year yields pared their decline to around 10 basis points by the close. He reaffirmed the Fed’s commitment to its inflation target and downplayed the June print as one data point rather than a finish line.

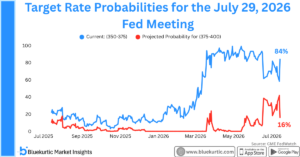

Expected Fed hikes fell across every month measured after the CPI release, from 0.45 to 0.17 for July, out to 2.15 versus 1.81 by next June. For the July 29th meeting specifically, the odds of a hold now sit at 84%, versus 16% for a hike, pulling back from the highs that built earlier this year.

The bigger picture still favors the bulls here. Rate expectations are easing, and the market has consistently found a way to look past shocks and grind higher through this cycle. The one thing worth watching is oil. Renewed fighting around the Strait of Hormuz is pushing crude back up, and if that filters into the next inflation print, it could test how much patience the Fed, and the market, really has. For now, though, the direction of travel supports the case for new highs.

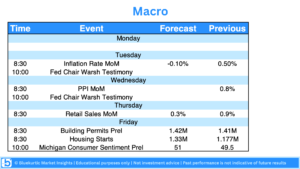

This week could be one of the most important of the summer for investors, with three major themes expected to drive market direction: macroeconomic data, the start of earnings season, and developments surrounding Iran.

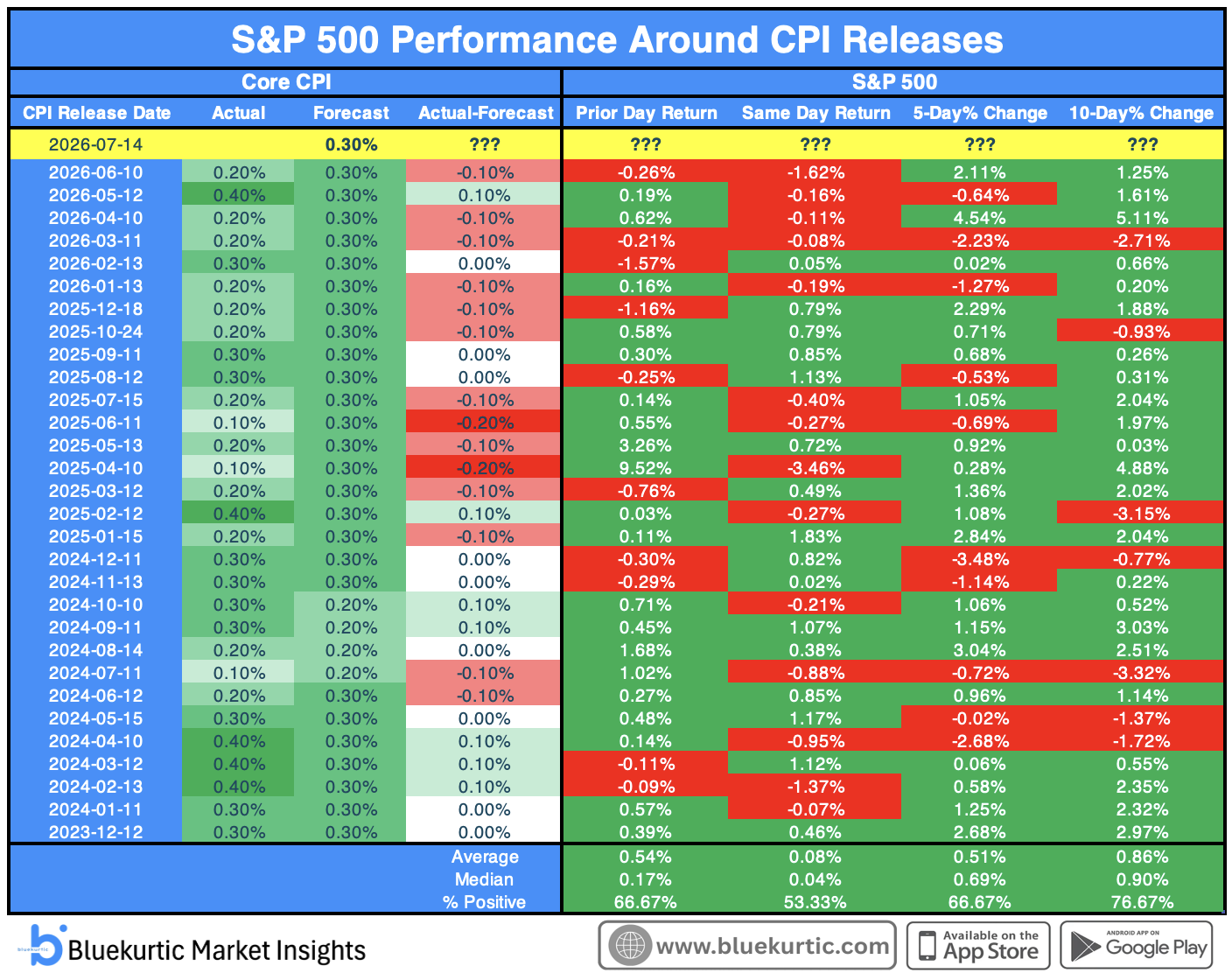

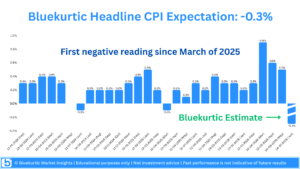

The biggest event arrives on Tuesday with the June CPI report, followed just ninety minutes later by Fed Chair Kevin Warsh’s testimony before the House Financial Services Committee. We believe inflation will set the tone for the rest of the week, as a softer-than-expected reading could encourage a more dovish message from the Fed.

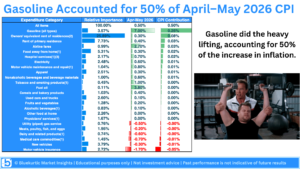

Our view is driven largely by energy prices. While headline CPI rose 0.5% in May, gasoline alone accounted for half of that increase. Since then, crude oil has fallen nearly 20% and returned to pre-conflict levels, which we believe should translate into lower gasoline prices and significantly reduce inflationary pressure. Our estimate calls for headline CPI to decline 0.3% month over month, which would mark the first negative monthly reading since March 2025.

A softer inflation print could also lead markets to reassess expectations surrounding Chair Warsh. We believe investors have interpreted his recent comments as more hawkish than intended, and a weaker CPI report could pave the way for a more balanced, or even dovish, tone.

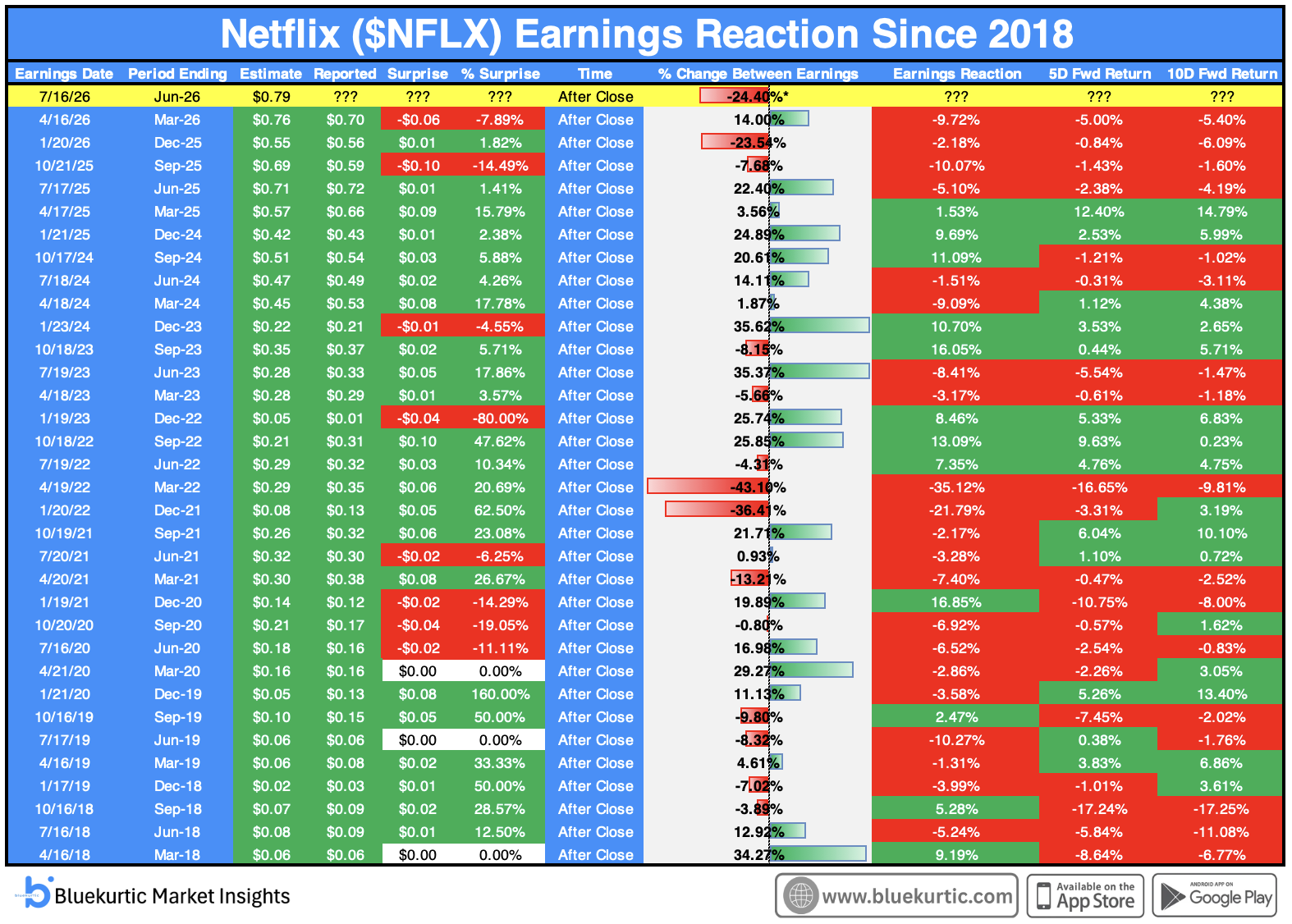

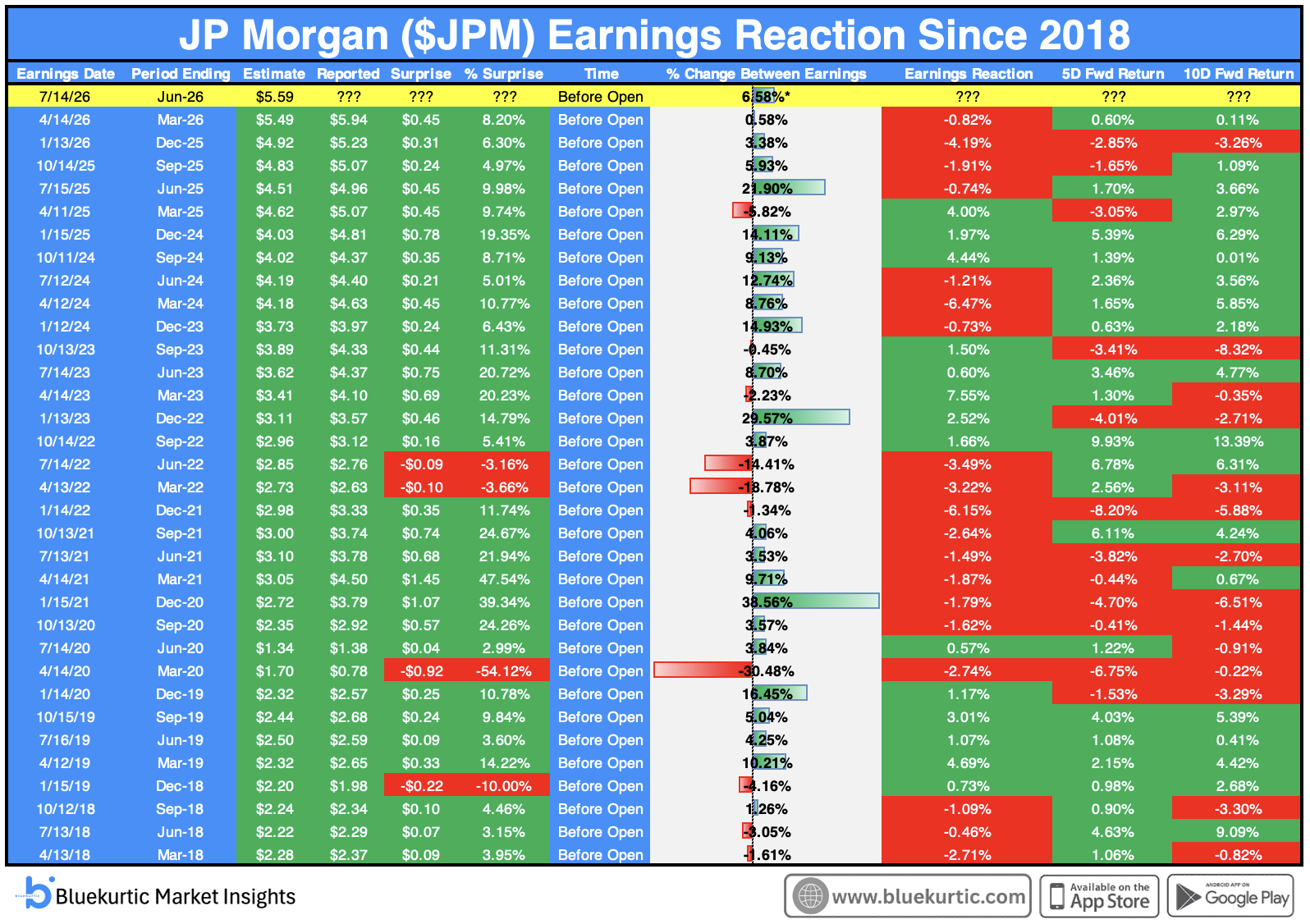

The second major catalyst is the start of earnings season. Large banks including JPMorgan, Citigroup, and Bank of America report on Tuesday, while Netflix headlines Thursday’s earnings after the close. As one of the first major technology companies to report, Netflix could set the tone for the broader tech sector.

From a technical perspective, the stock is approaching multiple long-term support levels, including prior resistance from before the 2022 bear market, its 200-weekly moving average, and a long-term trendline. While it’s impossible to call an exact bottom, we believe the current risk-reward profile has become increasingly attractive.

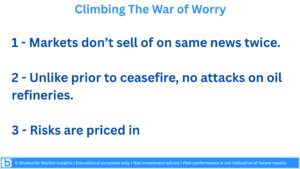

Geopolitics remains another key focus, but we believe markets continue to climb the “wall of worry.” The market has repeatedly absorbed negative headlines related to Iran with increasingly limited downside. Friday provided another example, as equities recovered within 44 minutes after an initial selloff following headlines suggesting the ceasefire had ended. In our view, this suggests much of the geopolitical risk has already been priced into markets. We also believe the current environment differs from earlier in the conflict, as attacks have shifted away from critical oil production infrastructure, reducing the potential for lasting supply disruptions.

Finally, technical and seasonal factors remain supportive. The S&P 500 recently triggered a bullish MACD crossover while trading near all-time highs—a setup that has historically produced favorable short-term returns. Seasonality also remains constructive, with July historically one of the strongest months for both the S&P 500 and Nasdaq 100, supported by the start of earnings season.

While short-term volatility is always possible, we believe the combination of potentially softer inflation, improving technicals, supportive seasonality, and the start of earnings season creates a constructive backdrop for equities as we move further into July.